The Government has introduced a Sustainable Aviation Mandate, which is a set of directions on how and when sustainable aviation fuel is to be introduced.

Neither “SAF” nor “Sustainable Aviation Fuel” are defined in the Sustainable Aviation Mandate[1]. However, there are listed sustainability criteria that are required for sustainable aviation fuel. The fuel has to meet a minimum GHG (Greenhouse Gas) emissions saving threshold which is that the GHG emissions saving from its use must be equal to or greater than the minimum GHG emissions saving applicable to that fuel. The Government Guidance sets the minimum saving applicable as “a minimum GHG emissions reduction of 40% relative to a fossil fuel comparator of 89gCO2e/MJ.” [2]

“That fuel” applicable to the GHG savings is defined in a schedule in the Mandate and includes fuels from various sources. For example, “Wastes of biological origin, which are not wastes from agriculture, aquaculture, fisheries or forestry” are required to meet the “The GHG emissions saving threshold”. “Forest biomass, including residues from forestry or wastes from forestry” are required to meet the “GHG emissions saving threshold and the forest criteria”. The “forest criteria” is that harvesting is subject to regeneration and is not taken from wetlands or peat.

“Residues from agriculture or wastes from agriculture” are subject to the emissions saving criteria, “land criteria” and “soil carbon criteria”. “Land Criteria” allow any land except forest, nature protection, biodiverse grassland and wetlands. “Soil Carbon Criteria” means that “adequate monitoring or management plans are in place for the land concerned which address the impacts on soil quality and soil carbon of the harvesting of the relevant feedstock from that land”.

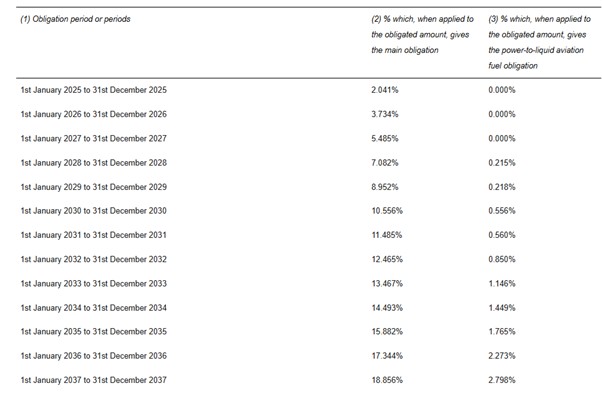

Strangely the Mandate does not seem to prohibit land previously used for food production. Indeed, the Government’s Guidance[3] under the Renewable Transport Fuel Obligation Order 2007 specifically states as a potential source “Products of biological origin, which include relevant crops and energy crops, and co products of biological origin arising as a result of production processes.” In short, dedicated crops for fuel production are permitted, even if taking up land that would otherwise be used for food production. However, fuels produced from crop-based feedstocks are not eligible for reward under the SAF Mandate. There is an obligation upon fuel suppliers to supply SAF, which will increase over time and the proportion of SAF supplied by a supplier and the amount of Power to Liquid is shown in a table in the Mandate, which is

The table above is calculated using a formula set out in the Mandate.

The SAF Mandate sets out extensive requirements to obtain “certification” of fuels so that they will be legally recognized as SAFs.

The Mandate states that the “minimum GHG emissions savings” required are the amounts determined by the government. The Government states that “all SAF must achieve a minimum GHG emissions reductions of 40% under the SAF Mandate. When fully replacing kerosene, SAF can achieve an average of over 70% greenhouse gas emissions savings on a lifecycle basis”.

The problem with the government’s statement of a 70% saving is that it can mean almost anything depending on how you use the savings figures and what you include. The Government’s Guidance states that:

“Sustainable aviation fuels (SAF) are fuels that reduce greenhouse gas (GHG) emissions from aviation over their lifecycle when compared to standard jet fuel. SAF can be made from a variety of feedstocks and can be easily blended with conventional jet kerosene for use in existing engines, with no modification for engines needed. There are 3 main pathways to create SAF:

-

- HEFA – HEFA (hydroprocessed esters and fatty acids) is a fuel developed from oils or fats, such as used cooking oil.

- Non HEFA – this pathway includes various methods of making advanced fuels from wastes and residues, such as fuel made from municipal solid waste.

- Power to liquid – this pathway includes fuels made from low carbon power sources, such as from renewable energy.”

The Government’s Guidance does not define “lifecycle”[4]. With biofuel crops the fuel is created from matter that has captured carbon during its growing period, whatever that might have been, and then the carbon is emitted when combusted by the aircraft on a flight. Set off one against the other and you are carbon neutral. Put in the emissions from conversion from biomass to fuel and you can end up with the figure of some 70% saving, which seems plausible. However, the biomass crops are grown on land that would have been used for food production in any case. So, there is, in reality, no net saving over using fossil fuel, since the carbon will have been captured by crops in any case. In the case of wastes used for SAF production, rather than biomass crops directly, the situation is a little different, but still misleading. If the waste were to be left to rot, it would emit carbon over a period. Food might decompose over say 6 months. Materials can take many years to decompose. During decomposition waste will emit its carbon in CO2. Waste will therefore emit CO2 in both situations, SAF combustion and decomposition. When combusted in a jet engine on a flight, the time for CO2 emissions is, say, 5 hours on a medium haul flight, rather than the rotting time of months or years. Comparing several years degeneration emission time with 5 hours emission time is like comparing apples with pears. The emissions from SAF will build up in the atmosphere far faster than allowing decomposition.

The only real saving from SAFs occurs where carbon is extracted either in itself or by CO2. This occurs with the “Power to Liquid” sector that the Government lists. However, with this sector the amount of energy to convert the CO2 into a SAF is considerable, negating at least some of the advantage. In addition, the Government’s proposed proportion of Power to Liquid is very small (4.487% by 2040 see above). Airbus describes the process, which is not new, as:

“In 1923, chemists Franz Fischer and Hans Tropsch decided to take a novel approach to converting coal into a new synthetic fuel – a process originally developed in Germany in 1913. Together, they tested an indirect way to liquefy coal in which solid coal is first transformed into a gas. The process involves introducing metal catalysts at temperatures of 150–300°C (302–572 °F) to set off a variety of chemical reactions resulting in liquid hydrocarbons – or a raw liquid form of carbon monoxide blended with hydrogen or water gas.” [5]

Airbus then goes on to summarise for modern times:

“PtL [Power to Liquid] is a synthetically produced liquid hydrocarbon. Renewable electricity is the key energy source, and water and carbon dioxide (CO₂) are the main resources used in PtL production, which consists of three main steps:

-

-

- Renewable energy powers electrolysers to produce green hydrogen.

- Climate-neutral CO₂ – captured via, for example, Direct Air Carbon Capture – is converted into carbon feedstock.

- Carbon feedstocks are synthesised with green hydrogen – via processes such as Fischer-Tropsch – to generate liquid hydrocarbons. They are then converted to produce a synthetic equivalent to kerosene”

-

Airbus say that the cost is high and the volume low at present, but that could change in the future. We could add that even if renewable energy is used, that is a finite resource and if it is taken up by the aviation industry trying to power itself, there will be less for other uses like power, heating and lighting, not to mention surface transport.

The Committee on Climate Change in its 2025 report to Parliament say that “the SAF Mandate came into force in January 2025, SAF deployment is increasing (2.1% in 2024), and the Sustainable Aviation Fuel Bill was introduced to Parliament in May 2025. We have therefore upgraded our SAF policy assessment for the 2030 NDC (AV01). Delivery risks remain for meeting the full 10% by 2030 SAF share target due to the various challenges facing supply, such as uncertain global SAF supply and diversifying away from HEFA. Currently, there are no operational UK SAF plants, but they are under construction and will be important for developing second and third generation SAF”.[6]

We shall see how the future pans out, but for now SAFs are not giving, or on target to give, the savings in carbon emissions claimed and should be treated with a large degree of scepticism.

.![]()

[1] The following documents are relevant to the Sustainable Aviation Mandate:

- Mandate at https://www.legislation.gov.uk/uksi/2024/1187/contents/made – The Renewable Transport Fuel Obligations (Sustainable Aviation Fuel) Order 2024

- Government website on SAFs https://www.gov.uk/government/collections/sustainable-aviation-fuel-saf-mandate . This includes a list of Guidance material issued by the Government

- Government Essential Guidance on SAFs https://www.gov.uk/government/publications/about-the-saf-mandate/the-saf-mandate-an-essential-guide

- RTFO and SAF Guidance https://assets.publishing.service.gov.uk/media/67626f161ca3ec0a49e1908e/rtfo-and-saf-mandate-technical-guidance-2025.pdf

[2] This is the amount of CO2 emitted per megajoule of energy produced – I megajoule = 1,000,000 joules and a joule is equal to the amount of work done when a force of one newton displaces a body through a distance of one metre in the direction of that force

[3] See at https://assets.publishing.service.gov.uk/media/67626f161ca3ec0a49e1908e/rtfo-and-saf-mandate-technical-guidance-2025.pdf

[4] Slaughter and May solicitors in their paper on SAFs at https://www.slaughterandmay.com/insights/new-insights/is-saf-taking-flight/ define lifecycle as “meaning all emissions associated with SAF production and use”.

[5] https://www.airbus.com/en/newsroom/news/2021-07-power-to-liquids-explained

[6] https://www.theccc.org.uk/publication/progress-in-reducing-emissions-2025-report-to-parliament/

Be First to Comment